The CZK class added +0.24 percent quarter-on-quarter, while the EUR class added +1.12 percent. The cumulative return from the beginning of the year to the end of Q3 was 3 percent in korunas and 4.84 percent in euros.

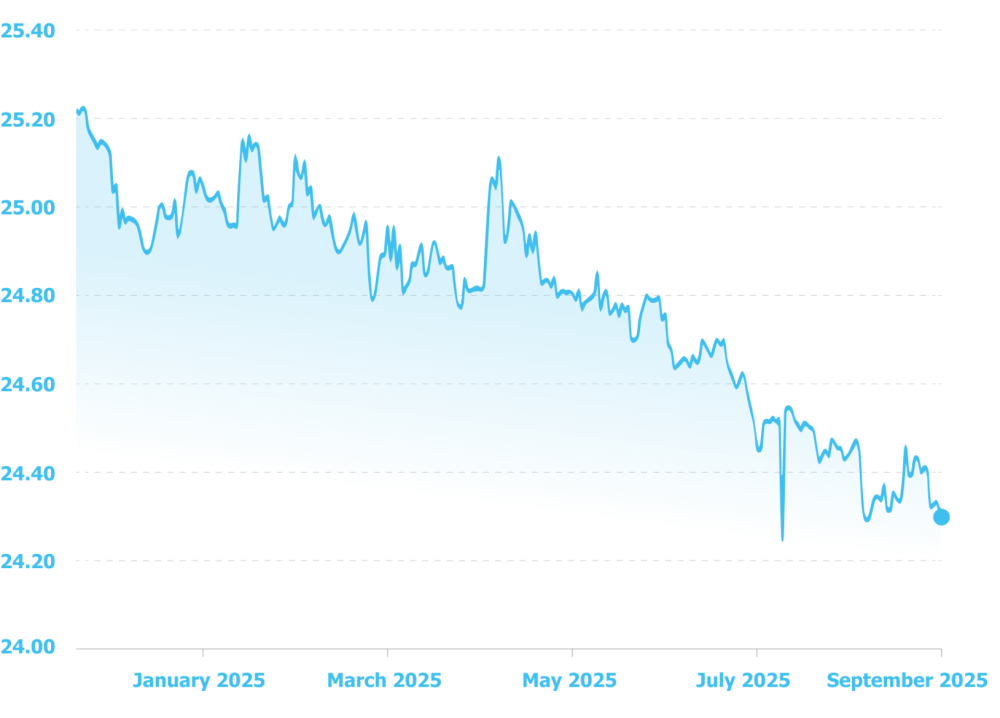

Two main factors stand behind these figures. The first is the continuing strengthening of the koruna. Just during this year, there has been a significant shift – while in January the exchange rate was approximately 25.3 korunas per euro, at the end of September it was 24.3 korunas per euro. A difference of one koruna may seem negligible at first glance, but given the size of the fund's portfolio, the overall impact is already very significant.

And while in the past decade, when the fund was smaller, it was possible to hedge currency fluctuations almost completely, today, given the amount of investments in Czech korunas, it is significantly more complicated. Our hedging strategy has mitigated the impact, but the resulting effect remains noticeable.

It should also be mentioned that this situation currently affects various other types of investments made in euros or dollars and settled in Czech korunas, where the strengthening koruna erases a significant portion of the profits from these investment instruments. However, we do not want to and will not use this as an excuse. Our intention is to increase the hedging ratio for the CZK classes, which currently stands at approximately 50%. We will also continue to search for additional partners for this type of transaction among banking houses and try to address the situation according to possible market development scenarios.

The second factor is the natural renewal of lease agreements, with a large number of contracts concluded between 2020 and 2022 coming to an end. The vast majority of them were successfully extended or the spaces were re-let, but some areas were temporarily vacated, leading to an increase in vacancy at the end of the quarter by just under one percent. As of the date of this newsletter's publication, we already know that in the fourth quarter, vacant space measuring 13,722 sqm in Accolade Funds Park Szczecin I was occupied by a new tenant. Thanks to this, the park is fully leased, which will be reflected in a reduction in the vacancy rate during Q4.

What is essential is that despite this development, we remain significantly below the market average: our current vacancy rate is 2.66 percent. In other words, more than 97 percent of our halls have tenants, and negotiations for vacant spaces are in full swing. For context – as part of the normal business cycle, approximately ten percent of areas in the portfolio are renewed annually. This can also be translated into an opportunity to negotiate higher rents, which we have been successfully doing in the long term.

Looking ahead, we remain optimistic. In locations where production and logistics make sense, there is a revival in demand. Data from both the Czech and Polish markets confirm that interest in modern, efficient, and ESG-ready spaces persists, although growth is more selective and focused on quality locations.

In conclusion, we would like to add that we see specific advantages in both the CZK and EUR share classes and are convinced of the prospects for both. We will continue to work honestly on developing our European portfolio, extending current contracts, and filling vacant spaces.